by Kelly KIRSCH

An ESG & Sustainable Finance Newsletter powered by ESG.AI

This week underscores a defining shift in global sustainability: ESG is not retreating — it is reorganising.

Europe is recalibrating its regulatory architecture under competitive and geopolitical pressure. Africa is institutionalising carbon disclosure through enforceable financial regulation. AI data centres are emerging as the new stress test for grids, water systems, and industrial strategy. Meanwhile, parts of the United States continue to distance themselves from collective climate frameworks, creating a more regionally fragmented ESG landscape.

The story is not about momentum slowing. It is about governance diverging — and capital adapting accordingly.

Here is your extended deep dive 👇

After sustained pressure from industry groups and diplomatic partners, EU member states formally approved amendments to the Corporate Sustainability Due Diligence Directive (CSDDD) and revised reporting thresholds under the Corporate Sustainability Reporting Directive (CSRD).

The result is a narrower, more politically durable framework — but not a dismantling of ESG governance.

CSDDD scope now applies only to:

· EU companies with more than 5,000 employees and €1.5 billion+ turnover

· Non-EU companies generating equivalent turnover within the EU

This significantly reduces the number of companies directly covered.

Compliance timelines extended:

· Implementation pushed to mid-2029, providing additional transition time.

Climate transition plan requirement removed:

· Companies are no longer required to adopt Paris-aligned transition plans under the directive.

CSRD reporting thresholds tightened:

· Reporting now applies to companies with >1,000 employees and €450M+ turnover

· Previously included companies with >250 employees

The revision reflects three intersecting pressures:

1. Competitiveness concerns — European firms argued compliance burdens could weaken global positioning.

2. Energy security sensitivities — The U.S. and Qatar raised concerns about potential disruption to energy supply chains.

3. Political sustainability — Policymakers sought a framework resilient to trade and geopolitical tensions.

Supply chain due diligence still carries enforcement risk. Fines can still be tied to global turnover. And large multinational corporations — the entities that shape global supply standards — remain squarely within scope.

Even with fewer companies covered, the largest players will continue to influence suppliers worldwide. ESG governance pressure will not disappear downstream.

This is regulatory concentration, not deregulation. The EU is focusing enforcement where it has the most leverage: large multinationals with systemic supply chain impact.

However, a secondary risk emerges: reduced CSRD coverage may weaken data comparability, making investor risk analysis more complex and potentially increasing reliance on estimates or third-party proxies.

The governance question shifts from “how many companies report?” to “how credible and comparable is the remaining data?”

· Large corporates: Use the delay to harden governance systems — supplier traceability, grievance mechanisms, audit-ready documentation.

· Mid-sized firms now outside scope: Expect indirect pressure from clients still covered by CSDDD. Prepare voluntarily.

· Investors: Adjust ESG screening models to account for thinner standardized reporting pools. Increase engagement-based diligence.

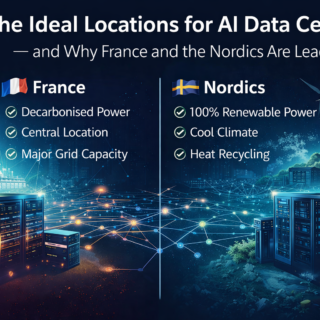

AI data centres are no longer peripheral technology assets. They are energy infrastructure, water infrastructure, and industrial policy instruments combined.

The ideal location is defined by four structural variables:

· Long-term low-carbon power access

· Grid interconnection certainty

· Cooling efficiency and water availability

· Permitting speed and community acceptance

Two European regions illustrate how this competition is unfolding: France and the Nordics.

Aurora Energy Research forecasts French electricity demand rising 74% by 2050, driven significantly by digitalisation and AI workloads.

France already hosts:

· 250+ data centres

· 11 GW of data centre capacity awaiting grid connection

Electricity use by data centres has:

· Tripled since 2019 (from 3 TWh to 10 TWh in 2022)

· Reached 2.2% of national electricity consumption

Demand characteristics:

· Intraday variation: ~5% (high stability)

· Seasonal variation: up to 23% (cooling-driven)

· Cooling may represent 40% of total energy use

France’s advantages:

· Stable low-carbon baseload (nuclear fleet)

· 20 submarine cable connections linking global traffic routes

· Improved efficiency (PUE reduced from >2.5 in 2007 to ~1.5 today; modern builds ~1.1)

France’s challenge:

· Grid connection timing and capacity coordination

· Managing cooling peaks during heat events

France is positioning itself as a continental AI hub — but execution will depend on grid readiness.

Sweden, Norway, Denmark, and Finland offer structural cooling and renewable advantages.

Notable projects include:

· Microsoft ($3.2B in Sweden) — ~1,000 MW new clean energy; 100% renewable operations

· Polar (Norway) — 12 MW AI-focused facility, renewable-powered, liquid cooling

· atNorth (Denmark) — heat reuse integrated into district heating

· Apple (Denmark) — renewable-powered European digital backbone

· LUMI (Finland) — hydro-powered supercomputer with waste heat reuse

Nordic advantages:

· Abundant hydro and wind

· Cooler climate reduces cooling loads

· Political stability and grid reliability

· Heat reuse potential for local communities

Nordic constraint:

· Transmission bottlenecks in some regions

· Distance from major continental consumption hubs (latency considerations)

AI data centres are becoming the next major ESG stress test.

Key emerging risk lenses:

1. Grid additionality — Is clean energy new or diverted from existing supply?

2. Water usage intensity — Cooling strategy under rising climate volatility

3. Peak load stress — AI demand coinciding with seasonal grid strain

4. Social license — Community perception of water and land use

PUE is no longer sufficient as a standalone metric. Investors will increasingly demand multi-dimensional performance disclosure.

· Developers: Integrate liquid cooling, demand-response capabilities, and heat recovery by design.

· Regulators: Require water usage transparency and grid impact modeling.

· Investors: Underwrite AI infrastructure with energy price volatility and climate resilience stress testing.

Ireland’s Circular Economy Strategy 2026–2028 positions circularity as industrial strategy, not environmental add-on.

Targets:

· Increase circular material use rate by 2 percentage points annually

· Reach 12% by 2030

Key actions:

· Repair Voucher Scheme (by 2027)

· Digital Product Passports (EU-aligned)

· Sector roadmaps across construction, packaging, textiles, electronics, food

Circularity reduces:

· Raw material exposure

· Import dependency

· Embedded emissions

It also creates new revenue models around repair, reuse, and refurbishment.

Circularity is becoming a hedge against geopolitical volatility. Companies that internalize material flows reduce exposure to supply shocks and price spikes.

The market is shifting from “recycling narrative” to “material strategy discipline.”

· Map material intensity and cost volatility exposure.

· Pilot product passport data architecture early.

· Investors: Treat circular metrics as operational efficiency signals.

Net Zero Asset Managers (NZAM) relaunched with 250+ signatories but softened requirements:

· No mandatory 2050 portfolio alignment

· No mandatory interim targets

· Self-determined target setting

Only 12 U.S. firms rejoined (down from 44). Some rejoined via European entities.

The shift reflects political risk management, not climate risk denial.

Climate risk remains financially material — but political risk is now co-equal. Asset managers must operate across divergent regulatory regimes while maintaining fiduciary defensibility.

· Separate climate risk management from political branding.

· Document scenario analysis rigorously.

· Asset owners: demand transparency on transition investment exposure.

Egypt’s Financial Regulatory Authority now requires non-bank financial institutions above EGP 100M capital threshold to:

· Report Scope 1 and Scope 2 emissions

· Verify through accredited bodies

· Offset ~20% of emissions via Egypt’s regulated voluntary carbon market

Market currently includes:

· ~170,000 carbon certificates

· 34 registered projects

· 8 accredited verification bodies

Non-compliance may affect licensing.

Egypt is institutionalising sustainable finance infrastructure through mandatory disclosure + market participation. This builds data credibility — the foundation for attracting global capital.

Africa’s climate finance ecosystem is moving from pilot phase to regulatory architecture.

· Institutions: establish emissions baselines early.

· Investors: assess integrity of offset verification systems.

· Policymakers: observe Egypt’s model as a replicable compliance-market hybrid.

This week’s pattern is unmistakable:

· Europe is refining sustainability governance, not abandoning it.

· Africa is embedding climate disclosure into financial regulation.

· AI infrastructure is rewriting the energy, water, and industrial playbook.

· The United States remains politically divided on ESG alignment.

We are entering an era of multi-speed sustainability — where governance frameworks vary by region, but systemic risks remain global.

Capital will flow toward resilience, regulatory clarity, grid stability, and credible data. The advantage will belong to institutions that can navigate fragmented regimes while maintaining disciplined risk management.

Sustainability is no longer ideological positioning.

It is infrastructure design.

🌍 #ESG #Sustainability

🤖 #AI #DataCenters #AIInfrastructure

⚡ #EnergyTransition #GridResilience

💧 #WaterRisk #CoolingEfficiency

🏛️ #EURegulation #CSRD #CSDDD

🌱 #CircularEconomy

🇪🇬 #Africa #CarbonMarkets

📊 #SustainableFinance #TransitionRisk

📈 #ESGAI #ClimateAnalytics

ESG.AI is now operating from Crédit Agricole’s Le Village Innovation Accelerator, 📍 55 rue La Boétie, 75008 Paris. A vibrant ecosystem where startups and corporates co-create solutions for innovation and sustainability—strengthening our mission to transform ESG reporting with AI across Europe.

About ESG.AI

If your business is navigating these developments, ESG.AI can help you stay ahead. From automating SME reporting to managing climate‑risk portfolios and supporting renewable‑energy investments, our platform uses cutting‑edge AI to turn ESG challenges into opportunities. Let’s connect to discuss how.

At ESG.AI, we’ve built a platform specifically for companies navigating the fast‑evolving landscape of sustainability regulation and reporting. It’s the only solution currently mapped against all major global ESG standards, giving organizations a unified framework for compliance and insight.

What sets ESG.AI apart is its agentic AI core. Our technology doesn’t just collect data; it acts on it—tracking your ESG metrics in real time, simulating “what‑if” scenarios and drafting regulatory filings so you’re always ahead of new requirements. As regulations proliferate, this proactive intelligence turns ESG obligations into opportunities for differentiation and strategic growth.

Through our strategic alliance with the London Stock Exchange Group, we combine deep regulatory foresight with cutting‑edge AI innovation. Whether you’re reporting to investors or planning long‑term sustainability initiatives, ESG.AI equips you with the tools to manage risk, seize competitive advantage and lead confidently in the ESG era.

For inquiries or to request a free trial, contact Kelly.KIRSCH@esg.ai in English or French.

For more information on ESG.AI go to

and

ESG performance Analytics